���α༭��ţ�ָ�

�Ŷ�ά��

![]()

![]()

���� ����

����ժҪ����ɫ�����ѳ�Ϊ�����й�����ҵת�͵���Ҫ·�������������Ƽ����ߵ����������������ҵ�����������ƣ�������ɴ���ƽ��ʧЧ������Դ������Ť�������ĴӲ�˰�����빫˾����˫�ز��棬�ص�̽������������߹ܼ�������ҵ��ɫ���µ�����Ӱ�졣�о���ʾ��н�꼤���Ĵ��²���ЧӦ�ܹ�������˰�������߶���ҵ��ɫ���µ�ƽ��Ч�������֮�£����������Բ�˰��������ɫ���¹�ϵ��Ӱ�첢��������н�꼤�������������Ļ�����ϵ�����˼�����ϵĴ��²���ЧӦ����н�꼤��ǿ�����е������£���˰�����ܹ�ʵ�ֶ���ɫ���µ������������á������ܹ��ӹ�˾�����ӽǽ�ʾ��˰����������۵ij���Ϊ�Ż�������˰���ߺ���ҵ���¼������ƣ��ƶ��й�����ҵ��ɫ��չ�ṩ��ѧ���ݡ�

�����ؼ��ʣ�������������ɫ���£�н�꼤������������

����1����

�����й�����ҵת�����������£���ɫ�����ѳ�Ϊ�ٽ���ҵ��������̬����Э����չ��ʵ������ҵ��ɫ��չ����Ҫ;��[1]��Ϊ������ҵ���ٵĴ�������Լ����������ط�������ʼ����ͨ����˰������֧����ҵ��ɫ���¡�Ȼ����������˰���ߵĴ���ƽ��ЧӦ�ܵ���ѧ��������ɡ����ܸ�ЧӦ����˵��Ϊ����˰�����Լ�����Χ�Ʋ�˰��Դ�ƶ���������������ƣ���������ҵ�����з�Ͷ��ʹ��¼�Ч[2]�����ң���˰�����ġ��źŴ��ݡ��롰��֤ЧӦ���������ҵ���ʱ��г��е��������������Լ�Ӳ��䴴����Դ[3,4]����Ҳ������ָ������������������ӿ��ή����ҵ�ҵ�ð�վ������ƴ��¼�Ч[5,6]�����⣬�ط������ġ����������������������ҵƭ����Ѱ�����Ϊ����������ʧ���Լ�������Դ�˷�[7,8]��

�������¼�Ч�IJ���������������ҵ����Դ����״̬�����ܵ������������Ը����Դ����Ч�ʵ�Ӱ�졣��ˣ�����������˰����������������¹��������Ⲣ�����ԴӸ�����������ҵ���¼�Ч����Ϣ���Գ������£��߹ܸ�����������������Դ��չ˽���ھ��Ƿ��սϸߵĴ��»[9]�����ң��߹ܱȹɶ��е��˸���Ĵ��·��գ�������������ֱ��ɶ�ռ�ݡ����²�����ȱʧ��һ�������˸߹ܴ�����Ը[10]����Ϊ��Ҫ�Ĺ�˾�������ƣ��߹ܼ��������ܹ���Ч����ί�д����ɱ������ܹ�ͨ���ṩ���²�������ķ�ʽ�����߹ܴ�����Ը����������˸߹�����ҵ�������ݵ���Ҫ��������ô�����ھ��л���Ч�õ�н�꼤���;�������Ч�õ���������[11,12,13]�����ּ������Ը������ڼ����߹ܵ���ɫ������Ը����߶���������������Ч�ʣ�

���������ص�̽����������������ɫ���µ�ƽ��Ч�������ڷ���н�꼤�������������Լ�������ϲ��ԵĴ��²���ЧӦ�Ļ����ϣ����Ͳ�ͬ�������ԶԲ�˰��������ƽ��ЧӦ�IJ��컯Ӱ�졣���ĵıʹ��������ڣ���һ���۽�����ɫ������һ���ش�����ʽ���ڷ������ֵ����ЧӦ�Ļ����ϣ���ʾ������������ɫ���µ�Ӱ�죬ͻ�����������Դ�����ʽ���з�����������ɵ��о��������ڶ����Ӵ��²����ӽǣ�����н�꼤������������˫�ز��濼�����������ƶ���ɫ���µ�ʵ���������Բ�˰�����Ĵ�����۽���ȫ�½��͡�������ȫ�濼�Ǹ߹����ٵ���ʵ�����龳������������ϲ��ԵĴ��²���ЧӦ��Ϊ����������������ɫ���µ�ƽ��Ч���ṩ��Ϊ�ḻ�Ĺ����㼤��������

����2����

����2.1�����

����2.1.1������������ҵ��ɫ����

������ɫ�������������Դ����Ч�ʺͽ��ܼ���Ϊ;������ʵ����ҵ��������̬������г��չΪĿ��Ĵ��»[14]����ҵ������ͨ����ɫ���մ��½��;��óɱ��ͻ����ⲿ��[15]��������������ɫ��Ʒ���з��������ҵ����Ч�뾺������[16]����ɫ���¶���ҵ��������̬������˫�ؼ�ֵЧӦ[17]���ܹ�����ط���������̬���ú�г��չ�ľ���Ŀ�꣬ʹ����г�ֵĶ�����������ԴͶ����ҵ��ɫ���»��2016�꣬�й�����Ժ����ί���������Ȳ�������ӡ���ˡ���ɫ��չָ����ϵ���͡���̬�������迼��Ŀ����ϵ��������ɫ��չָ�����������������ݣ������˵ط��������ò�˰������֧����ҵ��ɫ���»��������Ը��

����Ȼ����������Ϣ���Գƺ�ί�д�������Ĵ��ڣ��߹ܻ�����ô��¡���ͷ�������������������ⲿ��Դ�����������˽��[18,19]�������������㷺���ò�˰���ߴ����ƽ���ҵ��ɫ���µı����£���ɫ���ºܿ�����Ϊ�߹���˽���ĸ��˹���[20]���ɴˣ���˰�����ܹ�������ҵ��ɫ���µ�ǰ���������ڣ���������ҵ�Ĺ�˾���������ܷ�ʵ�ָ߹ܸ���Ŀ�꺯������ҵ���ڼ�ֵ��ͳһ����ʵ�ϣ�������ɫ���¶Ծ������ƺͻ�����Ч�����м�ֵ�������ã������������ڶ�����ת��Ϊ��ҵ�ɹ۲⼨Ч�����ң���Ϊ���·��յ���Ҫ�е��ߣ��߹�����ȡ���еĴ������棬�����Ҫ��ҵ��ƺ����ø߹ܼ��������Զ������������в�����

����2.1.2н�������������Ĵ��²���

�����߹�н���Ǹ߹���˾֧�����������������Ͷ��ľ������ã�������רҵ���顢������������˾��ȡ�Ļ������档��н�꼤����Ӱ���£��߹ܲ�������ͨ���������������ƶ���ѧ��Ч�ľ�Ӫ����[21]����������ʹ�߹ܴ��ƶ�ԭ�м����ĵͶ�����״̬������ͨ�����±������ɼ�ЧĿ�ꡣ����ɫ���¶��ԣ��߹�һ�����ܹ�ͨ����ɫ��Ʒ����������г���Ч����һ���������ù��մ�����������̬�ɱ����ⲿ���ƣ����ܾ�Ӫ�Ϸ��ԡ����䵱��ҵ��ò�˰��������������ɫ���������ڸ߹�˳����������Ի�����Ч�Ŀ���Ŀ�꣬�Լ�н�꼤����Լ���涨�ļ�ЧĿ�꣬������ø��˵Ĵ��²�����

��������������������������С������ͬ�к��˳ɾе�����Ч�ó�Ϊ�˼����߹�Ŭ��������ֱ������[13,22]��������ɫ���¶��ԣ��������������Ĵ��²���ЧӦʮ�����ޡ��ڲ�Ʒ���²��棬��ҵ��������Ҫ�������侭�ü�ֵ�����ϣ���ṫ�ڲ��������Ʒ����ɫ�������Զ�����ҵ����������������ۡ��ڹ��մ��²��棬��Ȼ��ɫ���մ����ܹ����ͻ����ⲿ�ԣ�����ҵ��������Ὣ�߹�����ɫ���մ��¹����и����Ŭ����Ϊһ�֡�����Ӧ����������ҵ��ȡ��������ı�Ҫ�ɱ��������ܹ�����������帣��ˮƽ�Ķ��ع��ס���Σ���ɫ���մ������ڶ�ʱ����ת��Ϊ���ü�ֵ�������ἷռ��Ʒ���з�Ͷ�룬�������г��Ļ���Ԥ�ڡ������ṫ�����ԶԸ߹��������������ԡ����ۡ��������Ϸ���������������裺

����H1a��н�꼤�����н�ǿ�Ĵ��²���ЧӦ��н�꼤��Խǿ��������������ɫ���µĻ���Ӱ��Խ������

����H1b����������ȱ�����²���ЧӦ������������������������ɫ���¹�ϵ�еĵ������ò�������

����2.1.3������ϲ��ԵĴ��²���

��������ҵ��ʵ�����龳�У��߹�ͨ�����ܵ����ּ������Ƶ�����Ӱ�졣�Ӽ������ṹ������н�꼤�������ж��ڼ������ƣ��������������ڳ��ڼ������ơ��Ӽ���ԭ��������н�꼤�����ھ���Ч���յ��µļ������ƣ����л����Ժ���Լ�ԣ�������������������Ч���յ��µļ������ƣ����зǻ����Ժͷ��ƶ��ԡ��ɴ˿ɼ������ߴ��ڵ��͵Ļ�����ϵ��

���������������������������кͳɾеȷǻ���Ч�ã�����Ч���ڸ߹�������������ռ�����ȵ�λ���߹���Ҫ������Ի���Ч������������£��Ż�����������������������Ч�á�����н�꼤��ǿ�ȵĸı䣬������ϲ��ԵĴ��²���ЧӦ��������̬�ݽ�����н�꼤��ǿ�Ƚϵ�ʱ��������ϲ�����������Ч�Ĵ��²�����������ɫ���·��շֲ��ڲ�Ʒ�з����������г������ȶ�����ڣ���Ҫ�ϸߵĻ��������������߹ܵķ��ճе�����һ�����������������ֲ���н��ˮƽ�����ļ�����ʧ�����²���ЧӦʮ����������н�꼤��ǿ�ȵ��������߹ܻ�õľ����������ӣ����������Ч�õIJ�������ת�������������������������ɾС���ʱ�����༤�����Ƶ�������ý�������ǿ�Ĵ��²���������н�꼤�����ڽϸ�ˮƽʱ���߹ܻ������Դﵽ��Լ�涨�ļ�����������չ������Ͷ�ʾ��ߣ������ػصͶ�����״̬�����ڻ������治����������������ЧӦ���������£���������������Ч�����Լ�����ҵ������Ը��������ϵĴ��²���ЧӦ�ٴ��½����������Ϸ���������������¼��裺

����H2a����н�꼤����������ˮƽʱ����ɫ���²���ЧӦ������������������ǿ����ǿ��������������ɫ���µĴٽ�ЧӦ����������

����H2b����н�꼤�����ڽϸ�ϵ�ˮƽʱ�����������ı仯���������ɫ���²���ЧӦ��������Ӱ�졣

����2.2����ѡȡ��������Դ

��������ѡȡ�ڻ����������е�����ҵ��ҵΪ�о�������2010�꣬�й����Ų���������ָ����Ҫ�ƶ�ר��滮�Ͳ�ҵ���߶��Ƚ�����ҵ�����з�֧�֡����ԣ����Ľ�ʱ��۲ⴰ����Ϊ2010-2017�ꡣ����δ������Ӫ�ġ�������������ȱʧ�Լ�ST���������ȡ��1134�����й�˾�����ݣ������˹۲�ֵΪ9072��ƽ��������ݿ⡣���У���ɫ������ʵ�����ͺ�������ר���ɱ������й�ר��ȫ�����ݿ��ֹ��ռ����á������������������ɱ��߸������й�˾����߹ܼ�������ɸѡ���������á��������ݾ���Դ�ڹ�̩�����й�˾���ݿ⡣

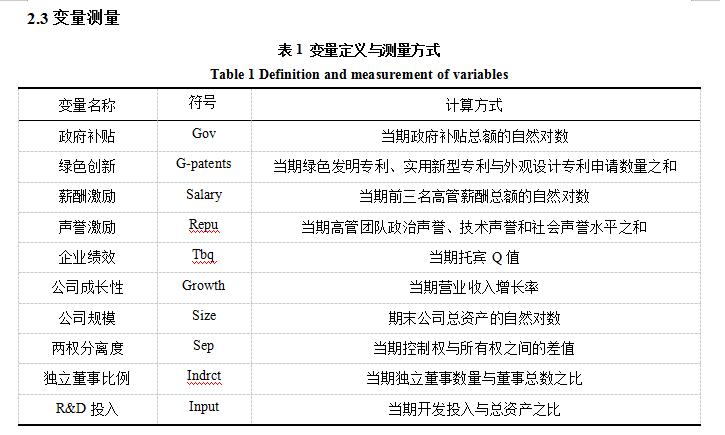

����2.3.1��ɫ����

��������������ù�ҵ�����ŷ���[23]���ߵ�λ�ܺĵ��²�Ʒ����������������ɫ����[24]��������Ϊ�������в����������ǵ��˲�ҵ������ܺĺ���Ⱦ�ŷ����⣬���������ӽ��¹۲���ҵ֮����ɫ���µIJ��졣Ϊ�˷������о����ޣ������ǵ�ר����Ȩ�����ܵ�����������������ص�Ӱ�죬���Ľ���ı������ؼ���ץȡ������������ɫר����������������ɫ���¡����ȣ�����Rennings[25]��Kemp[15]��Ȩ�����ԡ���ɫ���¡������������¡�������̬���¡���ظ���Ľ綨��ץȡ�ܹ���ӳ��ɫ���º����⺭�Ĺؼ��ʡ�ͨ����Ӣ��˫���룬�����˰������������ܡ���̼��10���ؼ��ʵĴʱ���Ȼ����������˾�ڹ۲��������������ר��ȫ����Ϊ�ı�����������ɸѡ�������ؼ��ʵķ���ר����ʵ������ר����������ר���������ɫר�������˹�ɸ�飬�������ؼ��ʵ���������ɫ���·����ר�����ݣ�����߲������ȡ�

����2.3.2�߹ܼ���

���������������棬���ǵ��߹���������;���Ķ�Ԫ�ԣ����Ĵ�������������������Լ�רҵ������������������������������ˮƽ�����У���������������Ȩ��������Ӱ�����Թ���������ļ������á����IJ��õ�����ҵ�߹��Ŷ��У����λ������������Ź�Ա�ĸ߹���������С��˴������������ЭίԱ�����ݵ���Ա�������в��������������ӳ�˸߹���������ҵ�е��ϿɶȺ����Ӱ��������������ҵЭ���Լ�������»����֯�о��м�ְ�ĸ߹���Ա�������в�����רҵ����������Ҫ�̻��˸߹���רҵ����������ȡ�õijɾͺ�Ӱ���������õ��ڻ�á��Ƽ����½���������һ�Ͷ����¡���רҵ�����Խ����������ĸ߹���Ա�������в�����

����2.3.3������������������

�����������õ������������ܶ����Ȼ����������������[7]����ҵ��Ч���棬ѡȡ����ȫ�淴ӳ��ҵ���г���ֵ�Ͳ���Ч���б�Qֵ���в���[26]�����Ʊ������棬���Ľ��������������빫˾��������������Ʊ����飬���У���������������������Ȩ����ȡ��������±�������˾����������������˾�ɳ��ԡ���˾��ģ��R&DͶ�롣����������ͼ���1��

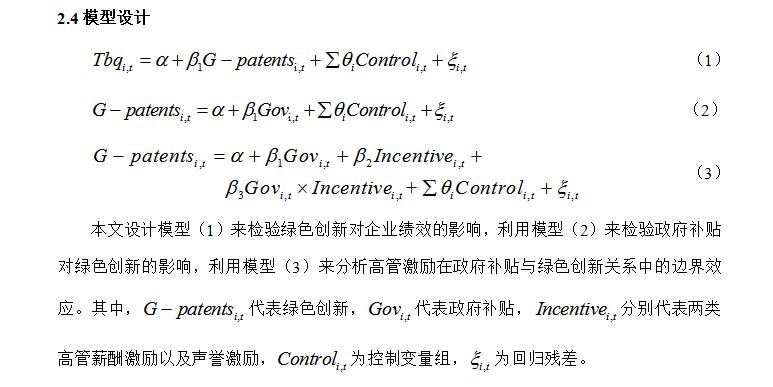

����3ʵ֤�������

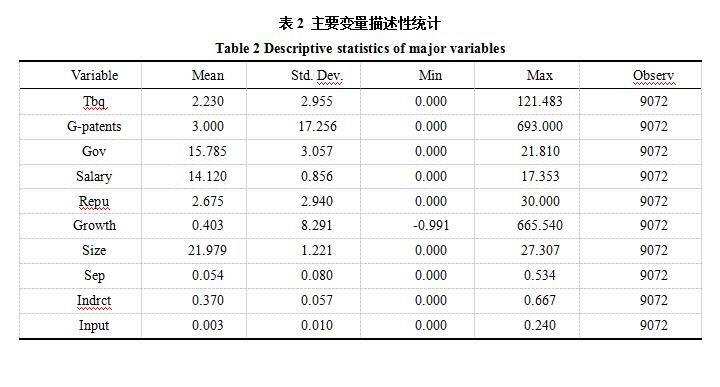

������2Ϊ��Ҫ������������ͳ�ƽ������ɫ����ר�������������ֵΪ693����СֵΪ0������Ϊ17.256��������ͬ������ҵ��ҵ����ɫ������Ը�ʹ��²���������нϴ���졣�����������ֵΪ21.810����СֵΪ0������Ϊ3.057�������ط������IJ�˰������ɸѡ���ƽ�Ϊ�ϸ���ҵ��ȡ�����������������ϴ����������������н�꼤�����������Խ�С������Ϊ0.856�����ֵΪ17.353����СֵΪ0������������˾�ձ����ӶԸ߹ܵ�н�꼤�����á����������������ֵΪ30����СֵΪ0������������˾����������ǿ�Ȳ���ϴ�

����3.2������������ɫ���µ�Ӱ��

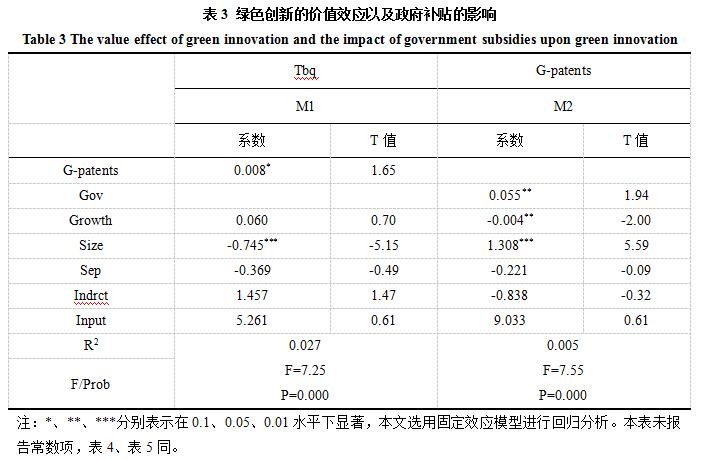

������3��������ɫ���µļ�ֵЧӦ��������������ɫ���µ�Ӱ����������ģ��M1�У���ɫ���±����Ļع�ϵ��Ϊ0.008����ͨ����0.1ˮƽ�������Լ��顣�ý��������ɫ����������������ҵ���弨Ч�����������ļ�ֵ����ЧӦ��M2�У����ͱ�����ɫ���µĻع�ϵ��0.055��������ˮƽΪ0.05������������������ɫ���¾��������Ļ����䶯��ϵ��������ϻع�����������ҵ��ɫ���µ�˫�ؼ�ֵЧӦ�����˵ط����������ú���̬������˫��Ԥ�ڡ���������������Ч�ֲ���ɫ��������֪ʶ����ͼ��������ɵļ��𣬲������ʱ��г��з��ӡ���֤ЧӦ��������ҵ����Լ�����ٽ���ɫ���¼�Ч��

����3.3н�������������IJ���ЧӦ

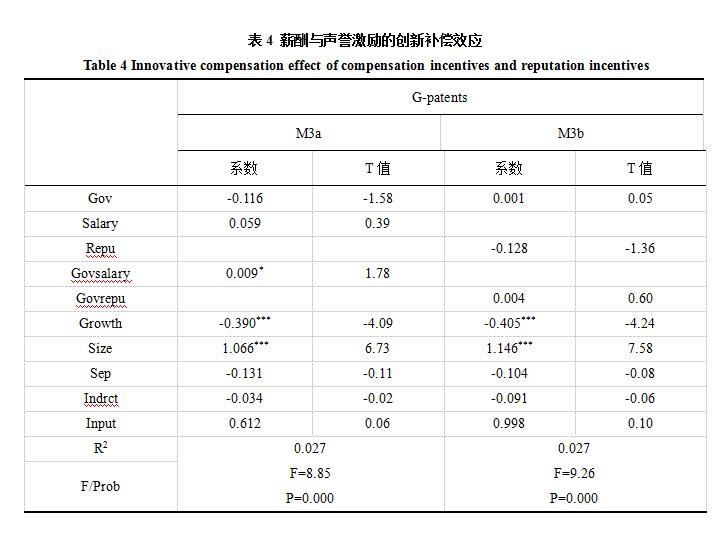

������4������н�꼤��������������������������ɫ���¹�ϵ�IJ��컯Ӱ�����������M3a�У�н�꼤�������������Ľ�����ع�ϵ��Ϊ0.009��������ˮƽΪ0.1������н�꼤�����ֳ������Ĵ��²���ЧӦ����ɫ���²���������ܺ�Ч�ʣ�ʵ�ֳɱ��������������������г���Ч���ٽ�����Դ������������ڸ߹ܴ�ɼ�ЧĿ�ꡣ����Ҫ�ģ�н�꼤�������Ĵ��²�����Ч�ֲ��˸߹ܵķ��ճе��������ȡ��ƥ����ʧ�⡣��˸߹ܾ��г�ֵĶ�������ȡ�IJ�˰����Ͷ�뵽��ɫ���»�У���ʵ�ָ�����������֯����Ĺ�Ӯ����ģ��M3b�У��������������������Ľ�����ع�ϵ��Ϊ0.004��Tͳ������Ϊ0.600����������������������Ч�Ĵ��²���ЧӦ����ṫ�ڶ���ҵ��ɫ����ս�ԵĹ��������¸߹������������Ч���ۡ�������ɫ���մ��µĶԾ��ü�Ч�Ĺ�����Ҫת��ʱ�䣬����ܼ�����ɫ��Ʒ�������������ԴͶ�룬�����˹������г��Բ�Ʒ�Ļ������ۣ��ϴ�̶��Ͻ����������Ը߹���ɫ������Ը�ļ������á�����H1a��H1b��֤��

����3.4������ϲ��ԵIJ���ЧӦ

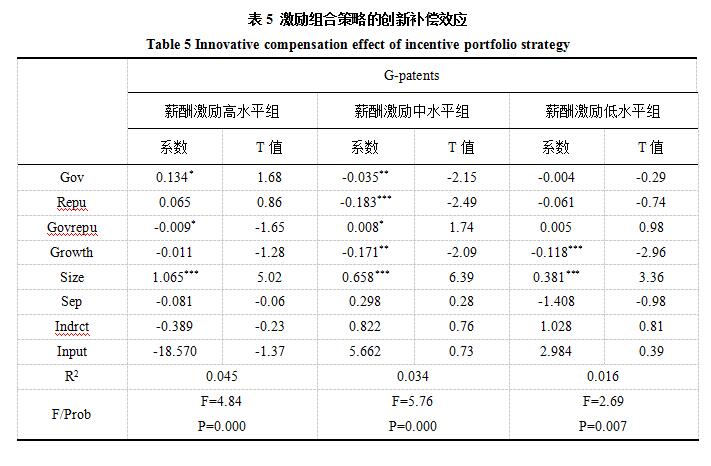

������5������н�꼤����������������ϲ��ԶԸ߹���ɫ���²���ЧӦ�ļ��������ڵ�н�꼤�����У��������������������Ľ�����ϵ��Ϊ0.005����δͨ�������Լ��顣����н�꼤��ˮƽ����ʱ��������ϲ��Զ�������������ɫ���µĹ�ϵӰ�첻���������²���ЧӦ����������н�꼤�������Ļ���Ч�ñ��������������ķǻ���Ч���и��ߵ����ȼ����������������н�꼤�������Ļ��Ҳ����������£�������Ը�������������Ч������������н�꼤�����У��������������������Ľ�����Ϊ0.008��������ˮƽΪ0.1��н�꼤��ǿ�ȵ����������˶Ը߹ܴ��·��ճе��Ļ��Ҳ������Ҹ߹ܿ�ʼ��ע���������ķǻ���Ч�ã����༤�����ƿ�ʼ���ӻ������á��ڸ�н�꼤�����У��������������������Ľ�����ϵ��Ϊ-0.009����ͨ����0.1ˮƽ�������Լ��顣����н�꼤��ˮƽ����ʱ������������������������ɫ���¹�ϵ�����˸���������á�н����Լ�涨��ЧĿ�������ѶȽϴ�ʱ�߹ܸ������ڽ�����������ս����Դ���õ��������϶̵�Ͷ�ʻ�У��Ӷ�������������ɫ���±�Ҫ���ʽ�Ͷ�룬��������ʹ�߹ܽ���Ͷ�����״̬��������������ɫ���¼�Ч������H2a��H2b��֤��

����4�о���������ʾ

������ɫ���µ�˫�ؼ�ֵЧӦ���й�����ҵ��ҵ��ɫ��չ������Ҫ���壬�������IJ�˰�����Ƿ����������˶���ҵ��ɫ���µ�ƽ�������Դ������顣�����ص�̽����н�꼤�������������뼤����ϲ��Զ�������������ɫ���¹�ϵ��Ӱ�졣�о���ʾ��

������һ��н�꼤�����������Ĵ��²���ЧӦ���ܹ���Ч����������������ɫ���µĻ���Ӱ�졣��ɫ���µ�˫�ؼ�ֵЧӦ�Ǹ߹�ʵ��н�꼤����ԼĿ�����Ҫ;������н�꼤�����ṩ�Ļ��Ҳ��������ܹ����Ƹ߹ܵĴ��·��ճе��봴�������ȡ��ʧ�����⣬�����ܹ���Ч�����߹ܶ����������ȴ�����Դ������Ч�ʡ��ڶ������������Ĵ��²���ЧӦ��������δ������������������ɫ���µ�ƽ��ЧӦ��������ṫ�ڼ���������������ڽ���ɫ���»��������ҵΪ��ȡ�������ѹ�������Ȳ�ȡ�Ĵ��¾��ߣ���˸߹���ͨ����ɫ��������������ۻ���������н��������������ϵĴ��²���ЧӦ������н�꼤����ǿ���̶ȡ�н�꼤�����ͻᵼ�¸߹�������ó�ֵĻ��Ҳ�����������ɫ���»��н�꼤��ǿ�ȹ��������´��¼������γɵͶ�����������н�꼤��ǿ������ʱ��н���������������ܷ�����Ч�Ļ���Ч�ã������߹ܶ����������ȴ�����Դ������Ч�ʡ�

�������Ķ����Ż�����ҵ��ҵ���¼������ƺ�������˰���߶���ɫ���µ�ƽ�����þ�����Ҫ������ʾ�����ȣ�Ӧ��ǿ�ط������Բ�����ҵ�ļල���������ƣ����Ͳ�˰���߶Թ�˾�ڲ����������������ԡ��ط�����Ӧһ���潨�����ڲ��������ʹ�����̵Ķ�̬��ܻ��ƣ���һ����Ӧ����ҵ��ɫ���¼�Ч����������ϵ����ʵ�����ҵ�Բ�˰����������Ч�ʡ����ߣ��Ż��߹ܼ�����Լ��ǿ���������Ƶ���ɫ���¼���ЧӦ������ɫ���¼�Ч��ΪĿ�꼨Ч����߹�н�꼤����Լ��������Ƹ߹ܷ��ճе��������ȡ��ʧ�����⡣Ҫ�������Ƹ߹��ھ������г��е�����������ϵ�����߹ܶ���ɫ���»�Ĺ�����Ϊ����ָ�꣬��ǿ������������ɫ���µ��������á�����Ӹ߹ܼ�������֮���ЭͬЧӦ�������Ը߹ܵ���ɫ���²�������ҵӦһ����Ȩ���趨н�꼤����Լ�е�ҵ������Ŀ�꣬������Ŀ��ʵ���Ѷȹ�����С����ɵļ���ʧЧ����һ����ͨ���Թ�������������ߵ��������������ı������ҵ��ɫ���µĹ���������������������ƵĴ��²���ЧӦ��

�����ο����ף�

����Ghisetti C, Rennings K. Environmental innovations and profitability: How does it pay to be green? An empirical analysis on the German innovation survey[J]. Journal of Cleaner Production, 2014, 75(14):106-117.

����Kleer R. Government R&D subsidies as a signal for private investors[J]. Research Policy, 2010, 39(10):1361-1374.

����Feldman M P, Kelley M R. The ex ante assessment of knowledge spillovers: Government R&D policy, economic incentives and private firm behavior[J]. Research Policy, 2006, 35(10):1509-1521.

����Takalo T, Tanayama T. Adverse selection and financing of innovation: Is there a need for R&D subsidies?[J]. Journal of Technology Transfer, 2010, 35(1):16-41.

����Wallsten S J. The effects of government-industry R&D programs on private R&D: The case of the small business innovation research program[J]. Rand Journal of Economics, 2000, 31(1):82-100.

����Duguet E. Are R&D subsidies a substitute or a complement to privately funded R&D? Evidence from France using propensity score methods for non-experimental data[J]. Social Science Electronic Publishing, 2003, 114(411007):245.

�������, ����Ȫ, �����, ��ΰ. ��ҵӭ����Ϊ������������Ч�о�����������ҵ��ͬӯ��״���ķ���[J]. �й���ҵ����, 2015(7):130-145.

����Zhao Can, Wang Zhu-quan, Yang De-ming, Cao Wei. Research on the catering behavior of enterprise and government subsidy performance: Based on the analysis of the enterprise��s profitability[J]. China Industrial Economics, 2015(7):130-145.

����������, ����, ������. ս�������˲�ҵ��������������ҵR&DͶ��[J]. ���й���, 2016, 37(5):19-23.

����Wu Xianyun, Chen Yan, Yang Weihua. A research on the effect of government subsidies on R&D investment of strategic emerging industries[J]. Science Research Management, 2016, 37(5):19-23.

����Wright M, Hoskisson R E, Busenitz L W. Firm rebirth: Buyouts as facilitators of strategic growth and entrepreneurship[J]. The Academy of Management Executive (1993-2005), 2001, 15(1):111-125.

����Low A. Managerial risk-taking behavior and equity-based compensation[J]. Working Paper, 2006, 92(3):470-490.

��������, ��ͮӧ, ����, ��ȫ��. �߹�н�꼤������ҵ�з�Ч�ʵ�Ӱ��ЧӦ�о�[J]. ���й���, 2015, 36(9):26-35.

����Chen Xiude, Liang Tongying, Lei Peng, Qin Quande. Influence of executive compensation incentives on corporate R&D efficiency[J]. Science Research Management, 2015, 36(9):26-35.

����Dale-Olsen H. Executive pay determination and firm performance: Empirical evidence from a compressed wage environment[J]. The Manchester School, 2012, 80(3):355-376.

��������, ������. ������ҵ�������ڵĸ߹ܼ�����Լ���Ŷ�̬���á�����ֵ������ӽ�[J]. ���������뾭�ù���, 2015, 35(6):80-93.

����Wang Xu, Xu Xiangyi. The optimal dynamic collocation of senior executives�� incentive contracts: An empirical study based on enterprise lifecycle theory[J]. Economic Theory and Business Management, 2015, 35(6):80-93.

����Jaffe A B, Palmer K. Environmental regulation and innovation: A panel data study[J]. Review of Economics & Statistics, 1997, 79(4):610-619.

����Kemp R. Eco-innovation: Definition, measurement and open research issues[J]. Economia Politica, 2010, 27(3):397-420.

����Driessen P H, Hillebrand B, Kok R A W, Verhallen T M M. Green new product development: The pivotal role of product greenness[J]. IEEE Transactions on Engineering Management, 2013, 60(2):315-326.

����Sharma S, Vredenburg H. Proactive corporate environmental strategy and the development of competitively valuable organizational capabilities[J]. Strategic Management Journal, 1998, 19(8):729-753.

����Hall B H, Harhoff D. Recent research on the economics of patents[J]. Annual Review of Economics, 2012, 4(1):541-565.

����Tong T W, He W, He Z L, et al. Patent regime shift and firm innovation: Evidence from the second amendment to China's patent law[J]. Academy of Management Annual Meeting Proceedings, 2014(1):14174.

��������, ���е�. ��ҵ��ɫ�������µĶ�̬�ݽ�:��Դ�����Ǽ�ֵ����[J]. �ƾ���ѧ, 2018(12):53-66.

����Wang Xu, Yang Youde. Dynamic evolution of business green technological innovation: Resource capturing or value creation[J]. Finance & Economics, 2018(12):53-66.

����Lazear E P, Rosen S. Rank-order tournaments as optimum labor contracts[J]. Social Science Electronic Publishing, 1981, 89(5):841-64.

��������, �����, ��ӱ. ���������Ķ���������Ϊ�о�[J]. �廪��ѧѧ��(��ѧ����ѧ��), 2012(1):129-136.

����Ning Xiangdong, Cui Bizhu, Zhang Ying. Research on the behavior of independent directors based on reputation[J]. Journal of Tsinghua University (Philosophy and Social Sciences), 2012(1):129-136.

�����Ž�ѩ, ����. ������ɫ�������ҹ���������ҵ��ҵ��������Ч���о�[J]. �������ü��������о�, 2012(2):113-125.

����Zhang Jiangxue, Zhu Lei. Research on technological innovation efficiency of industrial enterprises based on green growth on regions in China[J]. The Journal of Quantitative & Technical Economics, 2012(2):113-125.

����������, ����, ������. ����������������������ҵ��ɫ����[J]. ���й���, 2018, 39(1):26-33.

����Wang Fengzheng, Jiang Tao, Guo Xiaochuan. Government quality, environmental regulation and green technological innovation of enterprises[J]. Science Research Management, 2018, 39(1):26-33.

����Rennings K. Towards a theory and policy of eco-innovation-neoclassical and (co-)evolutionary perspectives[J]. Zew Discussion Papers, 1998, 35(1):23�C32.

����Ҧ����, ����, ��ѩ��, �����. �߹��Ŷ�ְ�������Զ���ҵ��Ч��Ӱ��:CEOȨ���ĵ�������[J]. �й�����ѧ, 2015(2)��117-126.

����Yao Bingshi, Ma Lin, Wang Xueli, Li Bingxiang. Functional diversity in top management team and firm performance: The moderating role of CEO power[J]. China Soft Science, 2015(2):117-126.

����No resource or no motivation? Government subsidies, green innovation and incentive strategy selection

����Wang Xu, Wang Fei

����(Business Administration School, Shandong University of Finance and Economics, Jinan 250014, Shandong, China)

����Abstract:With the overloading development of natural resources and the emergence of environmental problems, Chinese manufacturing industry needs to transform into an innovation-driven and green development model. Different from other forms of innovation, green innovation has positive significance for enterprises to cultivate competitive advantages and reduce environmental externalities, showing dual value effect. Thus, from the perspective of sustainable development, green innovation has become a crucial key to advance Chinese manufacturing industry to transform.

����In order to alleviate the innovative financing constraints faced by enterprises, the state and local governments began to focus on supporting green innovation through fiscal and tax policy. However, over-reliance on the exogenous influence of science and technology policies and neglecting the endogenous incentive mechanism of enterprises can easily lead to the failure of innovation smoothing and the distortion of public resource allocation. In this respect, this article from the both level of fiscal policy and corporate governance mainly analyzes the role of government subsidies and executive incentives upon green innovation. The issues discussed in this paper are new ones that have not been completely addressed by existing research. At the same time,manufacturing enterprises have a strong dependence on the dual value effect of green innovation, so this paper selects manufacturing enterprises listed in Shanghai and Shenzhen stock markets as research samples. Based on the perspective of corporate governance, this paper reveals the impact of compensation incentive, reputation incentive and incentive portfolio strategy on the relationship between government subsidies and green innovation.

����The research shows that although the green innovation activities are in line with the expected benefits of local governments on economic benefits and environmental performance, due to the existence of the principal-agent problem, the smoothing effect of fiscal and tax policy on green innovation depends on the innovative compensation effect generated by the executive incentive mechanism. Specifically, the findings of this paper suggest three main conclusions. Firstly, the innovative compensation effect of executive compensation incentive can improve the smoothing effect of fiscal and tax subsidy policy upon green innovation. Compensation incentive can force executives to break the low-end lock on the original technology and try to achieve performance goals through innovation. The dual value effect of green innovation is an important way for senior executives to achieve the goal of compensation incentive contracts. The monetary compensation provided by compensation incentive can not only improve the imbalance of innovation risk-taking and innovation income acquisition of executives, but also effectively improve the efficiency of executives' allocation of innovative resources such as government subsidies. Therefore, under the influence of salary incentive, senior executives have sufficient motivation to invest the obtained fiscal and tax subsidies into green innovation to achieve a win-win situation between personal income and organizational income.

����Secondly, executives cannot obtain innovative compensation from reputation incentive contracts, and reputation incentive has no significant impact on the relationship between fiscal and tax subsidies and green innovation. The psychological effects of reputation incentive, such as psychological satisfaction, social identity and personal achievement, are the direct incentives to motivate executives to work hard. However, since the public and stakeholders tend to attribute green innovation to the innovation decisions that enterprises are forced to make to obtain profits or reduce regulatory pressure, senior executives cannot accumulate reputation through green innovation. In addition, green process innovation cannot be transformed into economic value in a short period of time, and even squeezes the R&D investment of products, which reduces the positive expectations of the market. It is difficult for the public to have a ��dominant�� accumulation of executive reputation. Therefore, for green innovation, the innovation compensation effect brought by reputation incentive is very limited.

����Finally, the complementary relationship between compensation incentive and reputational incentive creates an innovative compensation effect of incentive portfolio. In the real decision-making situation, senior executives are usually affected by the integration of various incentive mechanisms. And under the condition of moderate compensation incentive intensity, fiscal and tax subsidies can realize the optimal driving effect upon green innovation. Compared with the non-monetary utility such as psychological satisfaction and sense of accomplishment brought by reputation, monetary utility takes priority in the level of executives�� psychological appeals. Therefore, under the condition of satisfying the executives' demands for money utility, the reputation incentive mechanism can play an effective incentive role. Since the risk of green innovation is distributed in multiple links, higher monetary returns are needed to compensate for the risk taken by senior executives. At the same time, too low salary incentives will cause executives to abandon green innovation because they cannot obtain sufficient monetary compensation. With the increase of compensation incentive intensity, the economic benefits of senior executives will increase, and senior executives will pursue the psychological satisfaction and sense of achievement brought by reputation. However, too high compensation incentive intensity may lead to conservative investment decisions by senior executives who cannot meet the incentive conditions in the contract. Only when the salary incentive intensity is moderate, can compensation and reputation incentive play an effective complementary role, and stimulate the allocation efficiency of senior executives to strategic resources such as government subsidies.

����This paper focuses on the smoothing effect of government subsidies on green innovation, and on the basis of analyzing the incentive effects of compensation incentive, reputation incentive and incentive portfolio strategies, explains the differential impact of different incentive strategies on the innovation smoothing effect of fiscal and tax subsidies. First of all, based on the analysis of the value effect of green innovation, this paper reveals the impact of government subsidies upon green innovation., and breaks through the research dilemma caused by the generalization of innovation form in existing literature. Secondly, from the perspective of innovation compensation, this paper examines the conditions for government subsidies to promote green innovation based on the dual levels of salary incentives and reputation incentive, and provides a new interpretation of the innovative paradox of fiscal and tax subsidies. Moreover, the research comprehensively considers the real decision-making situation faced by senior executives, and analyzes the innovation compensation effect of incentive portfolio strategy, so as to provide more abundant executive incentive schemes for improving the smooth effect of government subsidies upon green innovation.

����The final findings enable manufacturing enterprises to better optimize innovation incentives. Simultaneously, the findings provide a scientific basis for optimizing the government fiscal and tax policy, and will help promote the green development of Chinese manufacturing industry.

����Keywords:government subsidies; green innovation; compensation incentive; reputation incentive

���α༭��ţ�ָ�

�½��ٿ�������ƾ�ίԱ���ʮ�λ����ر�ǿ���˹�ͬ��ԣ�����Ŀ�꣬���ᶨ��ŵΪ�ˡ��������η��䡢�ٷ��䡢���η���Э�����Ļ������ƶȰ��š�����Ҫ�ؽ������η���ָ�������г��������������εĽ������ٷ��䣺һ��˰�շ�����Ϊ�����ٷ��䣻���ǻ��������������[��ϸ]

ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ǿ��������ʷΪ��������δ������������ƽ�����˼�����й������������۲����ϣ�ϰ��ƽ����˼����ϰ��ƽ��ʱ���й���ɫ�������˼�����Ҫ��ɲ��֣����й���ɫ������巨�����۵ļ��ɴ��£�������˼���巨��[��ϸ]

2020��11���ٿ�������ȫ�������ι��������飬ȷ����ϰ��ƽ����˼����ȫ�������ι��е�ָ����λ����Ϊϰ��ƽ��ʱ���й���ɫ�������˼�����Ҫ��ɲ��֣�ϰ��ƽ����˼��չ�ֳ���ѧ���ܵ����ܹ���ʵ��������������ʷ����ʵ�����ı�֤ͳһ��ϰ��ƽ����˼��������[��ϸ]

ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ָ��������ʷΪ��������δ����������о��������µ���ʷ�ص��ΰ������������Ҫ����ѧϰ�᳹ϰ��ƽ����ǹ��ڽ���ΰ������һϵ����Ҫ���������ڶ��������ڶ��������ﶷ��������߶������죬����սʤһ[��ϸ]

ʵ���л�����ΰ�����ǽ��������л�������ΰ������롣ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ָ������ʵ��ΰ�������Ҫ��ǿƴ������и�ܶ�����������������ܶ������ǵ��Ž�����й�������ΰ���·��������ΰ��ҵ��������ΰ��������[��ϸ]

ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ָ���������죬���DZ���ʷ���κ�ʱ�ڶ����ӽ����������ĺ�����ʵ���л�����ΰ���˵�Ŀ�꣬ͬʱ������������Ϊ��ޡ���Ϊ����Ŭ�������µ������ϣ����DZ��������ʶ��ȷ�����ⲿ��������̱仯���ҹ�[��ϸ]

ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ָ������һ����ǰ���й��������������Ǵ������й����������γ��˼���������������룬���г��ġ�����ʹ��������������Ӣ�¶������Ե��ҳϡ����������ΰ�����������й��������ľ���֮Դ����һ��������[��ϸ]

ϰ��ƽ���������ף�й�����������100�������ϵ���Ҫ������ָ���������Ǽ�ֺͷ�չ�й���ɫ������壬�ƶ������������������������������������������̬����Э����չ���������й�ʽ�ִ����µ�·��������������������̬�������Լ���·���ǵ���ȫ�����ۺ�ʵ������㣬[��ϸ]

���й��Ŵ�����������ʷ�У��Ƴ��������ް�ʷ�������顷�����顷�������顷�����顷�����顷�Լ������顷����ʷ������ʷ����Ԫ���������ޡ���ʷ������ʷ������ʷ�������ڳ�͢�����µ����δ��ģ��ʷ����������ù�ʮһ����ʷ�����ڽ�����������ʮ��ʷ���İ�����[��ϸ]

ѧʷ�����ǵ�ʷѧϰ��������ŵ㣬Ҫ��ѧʷ������ѧʷ���š�ѧʷ��µijɹ�ת��Ϊ������������Ϳ������ʵ���ж�������Ҫ���ѧʷ���У���ѧϰ��ʷͬ�ܽᾭ�顢������ʵ���ƶ��������������ͬ������ѡ�������Ϊ��������������������ؽ�ȡ�����в�ꡣ��ÿ��ʵ[��ϸ]